Article 3 of 5 | Following our May 2026 Chartwell webinar

The gap between struggling and seeking help

US utility arrears balances have surged 40% since 2023, now sitting at $25 billion. Collections processes are more mature than they’ve ever been. And yet the debt keeps rising.

At the same time, something else is happening. Something that doesn’t get enough airtime.

More customers are falling behind. Fewer are accessing support.

Data from the Smart Energy Consumer Collaborative shows that 44% of customers now report making a late payment, up from 39% in 2023. But only 17% have applied for an assistance program, down from 27%. The gap between struggling and seeking help is widening, not closing.

If the problem were simply awareness, that gap would be closing. Programs exist. Information exists. Most utilities have invested heavily in both. And still, silence.

So what is actually going on?

The psychology behind the silence

Rebecca Wilson, a Business Psychologist at SmartMeasures, put it plainly in the recent Chartwell webinar: “The reason people don’t reach out is not that they don’t know. It’s how financial stress makes them feel and what that does to their behaviour.”

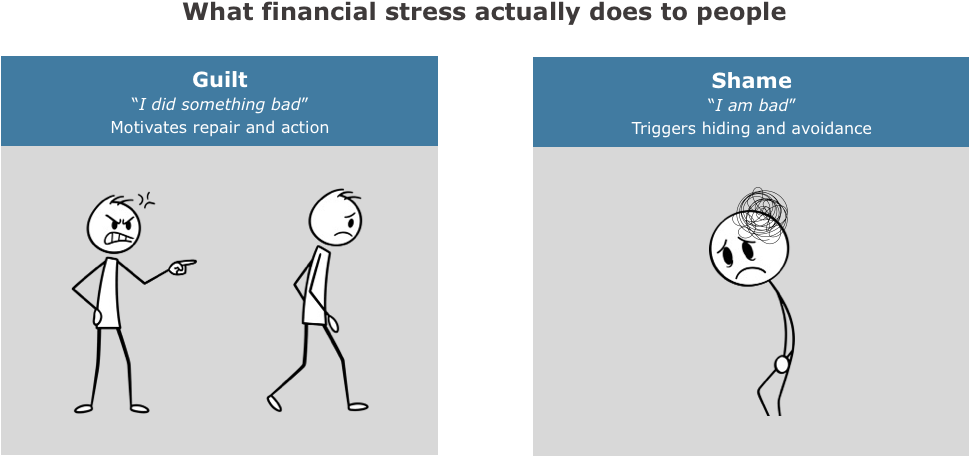

The key to understanding that, is a distinction that most outreach strategies overlook entirely: the difference between guilt and shame.

Guilt says I did something bad. Shame says I am bad. They feel similar from the outside but produce completely opposite behaviours. Guilt motivates repair. Shame motivates hiding, avoiding anything that might confirm the feeling.

For a customer who has just missed their first bill, contacting their utility is an act that could confirm their worst fear about themselves. So they don’t. Not because they’re difficult or disengaged. Because their brain is protecting them.

There is a second mechanism at the neurological level. Financial stress activates the brain’s threat response. The prefrontal cortex, responsible for planning, evaluating options and making decisions, effectively goes offline. A customer in that state can receive a perfectly clear letter about an available support program and be genuinely unable to act on it.

The result is what Rebecca describes as the shame spiral: missed payment leads to shame, shame leads to avoidance, avoidance allows the situation to worsen, and a worse situation produces more shame. Each missed bill makes the next contact harder to respond to. The window for effective intervention narrows every time.

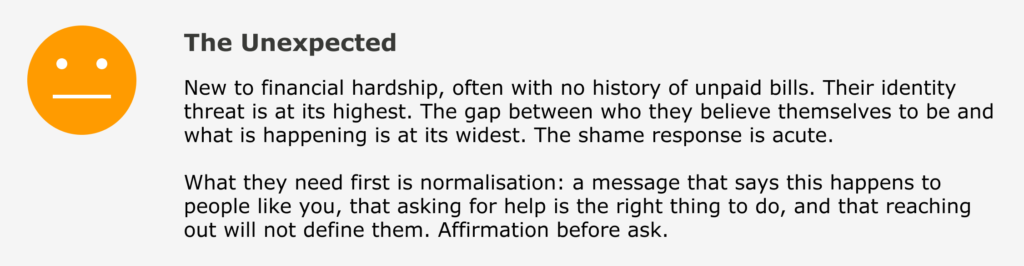

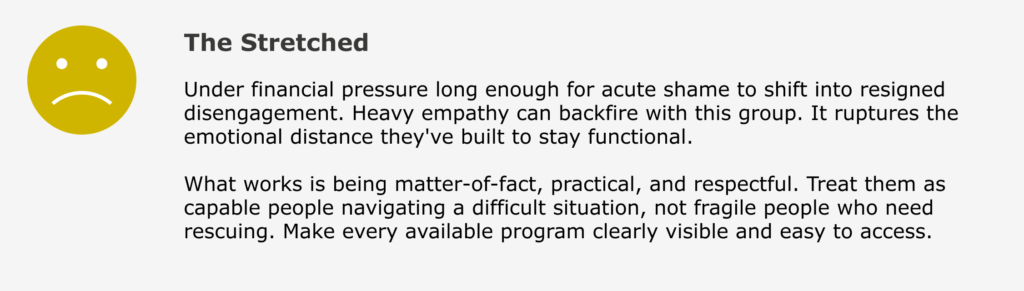

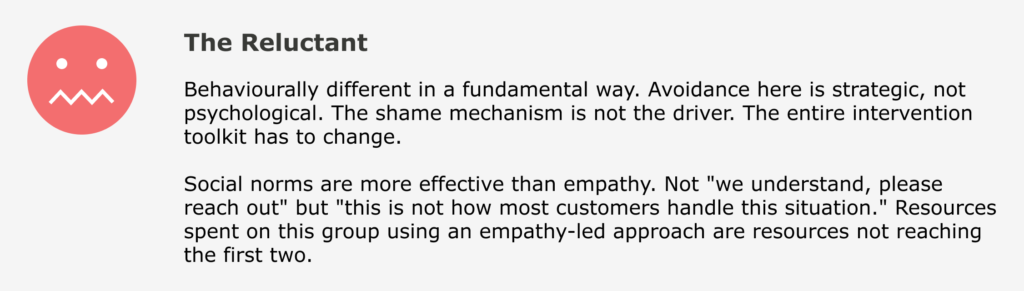

Not all disengaged customers are the same

The psychology driving disengagement is not uniform. It plays out in at least three distinct patterns. Each one requires a fundamentally different response.

This is why more outreach, sent through the same channels in the same tone, doesn’t change the outcome.

As Rebecca noted: “Use one message, one tone, one channel — and you’re almost certainly wrong for two out of three of those groups.”

The intervention must precede the spiral

Reflecting on Rebecca’s framework, Pat Ricks of Chartwell’s Vulnerable Customer Leadership Council, who has spent 36 years working in utility customer experience, noted that catching customers early enough in the process changes their experience of the interaction entirely, shifting them from feeling like they are receiving a handout to feeling like they are part of the solution.

That is not just a customer experience observation. It is a psychological one. Reach a customer before shame has taken hold and you are having a different conversation with a different brain. Wait until they are 90 days past due and the shame spiral has been running for months.

The shift that matters

More collections activity is not the answer to rising arrears. The data from the past two years is clear on that. The activity is there. The processes are mature. What has been missing is a precise understanding of who is on the other end of that outreach and what psychological state they are in when it arrives.

Utilities that are beginning to close the gap between struggling and seeking help are not sending more messages. They are sending different ones, to the right people, at the right time, designed around the psychology rather than the process.

That is the shift. And it starts with understanding that a missed payment is not a single event. It is the beginning of a story and the opening chapter tells you almost everything you need to know about how it ends.

#Utilities #CustomerExperience #BehaviouralScience #Collections #Arrears #EnergyUtilities #AI #FinancialStress

SmartMeasures helps energy retailers and utilities reduce customer debt and improve retention through predictive AI and behavioural science. To continue the conversation from the webinar, contact us here.

Rebecca Wilson MSc (Business Psychology) is a Business Psychologist and Behavioural Science specialist at SmartMeasures.