Article 1 of 5 | Following our May 2026 Chartwell webinar

This article follows our recent Chartwell webinar, and is part a series of thought leadership articles based on the themes we discussed, including early identification of financial stress, customer engagement, and behavioral approaches to reducing arrears.

US utility arrears have surged by 40% since 2023, now totalling around $25 billion.

Average household utility debt has risen from roughly $600 to $800. And collections teams are working harder than ever.

That combination of more effort and worse outcomes is the tension at the heart of the utility debt problem right now. And it deserves a direct answer.

“We’re doing more. The outcomes aren’t following.”

Pat Ricks has spent 36 years working in the utility customer experience field. As the voice of Chartwell’s Vulnerable Customer Leadership Council, a group representing utilities across the US, Canada and Puerto Rico, he has watched this problem develop in real time.

His framing at our recent webinar was not a criticism of the industry. It was an honest diagnosis.

Collections processes, he noted, have never been more developed. Utilities have experienced teams, refined workflows, flexible payment options and stronger hardship programs than they had a decade ago. Many have absorbed the lessons of the pandemic. Support exists. Communications have improved. The effort is real.

And yet, the data tells a different story.

These are not immature organisations flying blind. These are utilities with established infrastructure and genuine commitment to customer support. When experienced organisations running mature processes still report poor outcomes at that rate, the problem is not a lack of effort. Something structural is missing.

The debt isn’t just growing. It’s deepening

Part of what has changed is the nature of the debt itself. When a customer misses a single payment and catches up next month, the collections process works exactly as it should. It’s that instance that it was designed for.

But a growing share of customers are not carrying one missed bill. They are carrying multi-month balances that have compounded over time. Once debt reaches that level, something shifts. For the customer, the balance starts to feel insurmountable. For the utility, the available levers narrow. Conversations become harder. Outcomes cost more to achieve and are harder to sustain.

This is the trap that mature collections alone cannot escape. A process built to respond to debt cannot easily prevent the conditions that create it.

The priority has shifted — and the council saw it coming

Something telling happened in Chartwell’s council conversations leading into 2025. For several years, the primary focus had been identifying and engaging vulnerable customers. That remained important.

That is not a subtle distinction. It is a fundamental reorientation of where the problem needs to be solved.

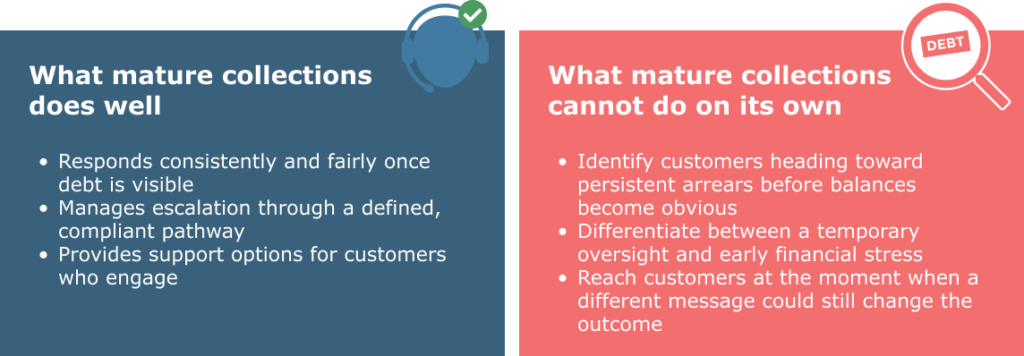

Most utilities, as Pat put it, are genuinely good at the bottom of the cliff, supporting customers once they have fallen, managing hardship, working through difficult conversations. That capability matters and should not be underestimated. But the bottom of the cliff is an expensive, difficult place to operate. The opportunity and emerging priority is to catch more customers at the top before the fall begins.

That requires seeing something that standard collections processes are not designed to see.

What collections can do, and what it can’t

Collections processes are built around events. A payment is missed. A message is triggered. If the account remains unpaid, activity escalates. That logic is fair, consistent and compliant. It has to be.

But event-based systems have a structural limitation: they respond to what has already happened. They are less able to distinguish what is likely to happen next.

From the outside, two customers with a first missed payment can look identical. One is dealing with a timing issue: the payment will come, the standard reminder will work, and the matter will resolve itself. The other is at the beginning of a pattern that will become persistent debt. Their balance does not look alarming yet. Their account history may be fine. But the trajectory is already diverging.

Traditional collections puts both of them on the same pathway. That is the hidden flaw in the model.

We need a new question

The industry has spent years asking: How do we collect more effectively?

That question still matters. But it is no longer sufficient.

The question utilities now need to answer is: How do we reduce the number of customers who reach collections in the first place?

Closing that gap requires two things working together: predictive AI to identify early-stage financial stress in existing data, and behavioural insight to determine what to do once a higher-risk customer has been identified. Because — as the next articles in this series explore — the barrier that stops struggling customers from engaging is not just a process problem. It is a psychological one.

Where this series goes next

This article sets up the problem. The articles that follow go deeper on each part of the answer.

- Article 2: Examines the first missed payment in detail: why it is the most important moment in the customer journey, and why most utilities treat it the same way regardless of who is behind it.

- Article 3: Explores the psychology: why customers in financial hardship go quiet, what shame has to do with it, and what it actually takes to reach them.

- Article 4: Looks at the predictive model: how early-stage financial stress leaves traces in operational data, and how AI identifies them at scale before arrears become entrenched.

- Article 5: Profiles what leading utilities are already doing differently, and what the shift from collections to prevention looks like in practice.

Utility debt keeps rising not because the industry is failing. It is rising because the environment has changed, customer pressure has intensified, and the tools that have served the industry well were built for a different version of the problem.

The next frontier is not better debt recovery. It is getting there before the debt exists.

SmartMeasures helps energy retailers and utilities reduce customer debt and improve retention through predictive AI and behavioural science. To continue the conversation from the webinar, contact us at [email protected] or contact us.

Rebecca Wilson MSc (Business Psychology) is a Business Psychologist and Behavioural Science specialist at SmartMeasures.