Article 5 of 5 | Following our May 2026 Chartwell webinar

The gap between theory and practice

The case for debt prevention is straightforward. Identify customers heading toward persistent arrears before the balance becomes significant. Match the intervention to the customer’s actual psychological state. Measure what changes. The logic holds at every step.

But utilities are not short of compelling counter arguments. They are short of evidence that a given approach will work in their environment, with their systems, within their governance frameworks, and at the scale they operate.

That is the test that matters. And as Eric Alam from Skipping Stone, our U.S. partner, noted in closing the Chartwell webinar, financially stressed customers are not going to self-identify. The utility has to act on what it already knows. Waiting for customers to come forward is not a strategy.

It is a hope. And hope is not much of an operating model.

Starting with scepticism

The program described here ran at ENGIE, an energy retailer operating in Australia, a market that mirrors the US in its arrear’s trajectory, regulatory pressure, and the widening gap between customers in financial stress and those accessing support.

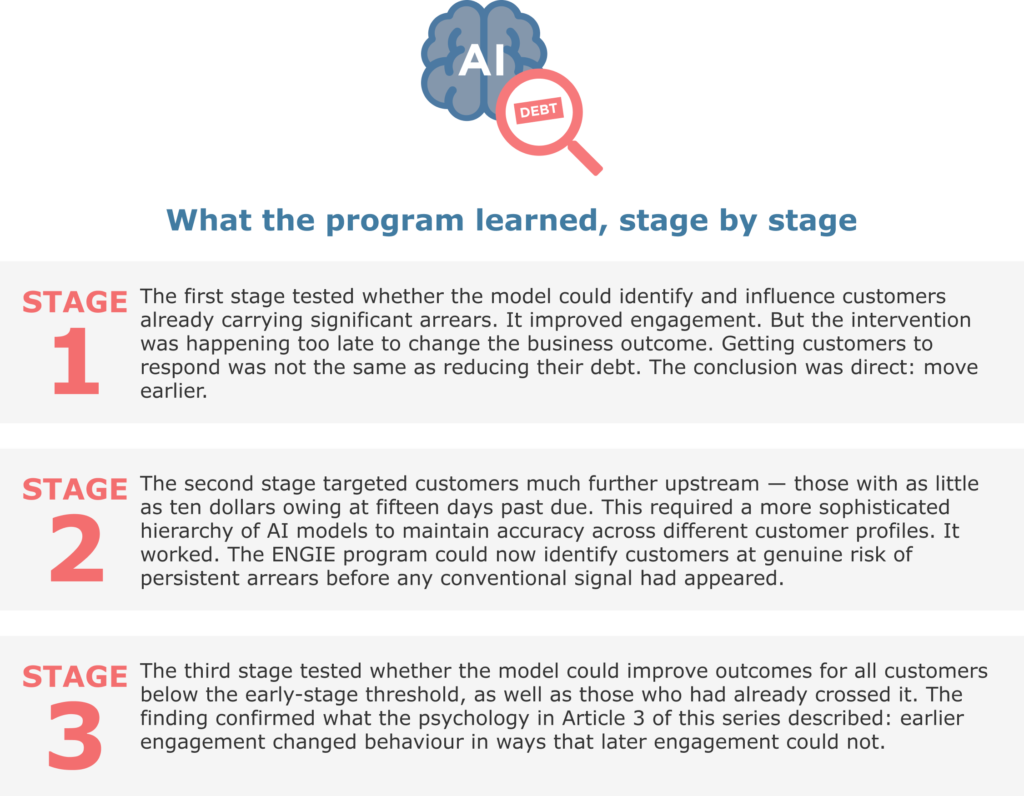

The program’s ambition was specific: to reach customers earlier in the collections cycle, before significant arrears had accumulated. The starting position was honest. The organisation had seen predictive models for collections pitched before. None had delivered. The question was whether this one would be different.

The answer came in three stages.

For customers reached before arrears had compounded, engagement improved meaningfully and in some customer profiles dramatically. Business performance followed. Arrears were reduced and cleared at significantly higher rates than in the control group. For customers already past the threshold, engagement also improved. This didn’t, however, translate into the same business performance gains. The debt had grown large enough that contact, without the ability to fully resolve it, produced engagement without resolution.

What the data confirmed

The results were consistent with something that runs through every article in this series: timing changes everything.

Not because collections teams work less hard at later stages. Rather, it’s because of what the psychology does to both the customer and the conversation as time passes. The shame spiral described in Article 3 is not a metaphor. It is a process. Each missed bill makes the next contact harder to respond to. Each month the balance grows, the customer’s sense that the situation is resolvable shrinks. By the time a customer is 90 or 120 days overdue, shame, avoidance, or resignation have often already taken hold. The organisation is still able to help but the intervention is later, harder, and more expensive.

The program also confirmed something equally important: early intervention did not just recover existing debt. Customers who engaged early, even partially, even with a small payment or a plan, were less likely to fall into deeper arrears later. The prevention layer was reducing the volume arriving at the bottom of the cliff, not only assisting those already there.

And it ran in parallel with normal collections activity throughout. Nothing was replaced. The existing process continued with the prevention layer operating alongside.

What the shift requires

It does not require new systems. The ENGIE program ran on operational data the utility already held — billing history, payment behaviour, service interactions, and the signals the utility itself generates every day.

It does not require certainty upfront. The program took three iterations to reach the design that worked. That is not a failure of the model. It is how evidence-based programs are supposed to run. The first stage taught the team something the second stage could use. The iterative weekly rhythm — refresh the data, test new treatments, measure continuously — is not a temporary phase. It is the operating model.

This way of working requires a different definition of success. Not only how much debt was recovered, but how much avoidable debt was prevented. Not only how many customers were contacted, but how many changed course before the account escalated.

And it requires the organisation to accept what Article 2 in this series established: the moment of first missed payment is when every customer still looks the same on the surface while being the most different underneath.

The image that closes this series

That image has framed every article in this series. Article 1 established that utilities are genuinely good at the bottom of the cliff — the hardship conversations, the structured payment plans, the difficult work of supporting customers who have already fallen. That capability matters. It should not be underestimated and it should not be abandoned.

But the bottom of the cliff is an expensive place to operate. The conversations are harder. The options are narrower. The customer’s sense of agency is at its lowest point. The shame spiral, as Article 3 described, has been running for months.

The shift this series has described is not about replacing what happens at the bottom. It is about deploying more intelligence at the top — so that fewer customers arrive at the bottom having already lost hope, and more of them are reached at the moment when the path can still change.

That is the difference between managing a debt problem and preventing one. The evidence now exists that it can be done.

We help energy retailers and utilities reduce customer debt and improve retention through predictive AI and behavioral science.

For utilities exploring how to identify early-stage financial stress sooner, a low-risk Proof of Value pilot can test the approach using your existing data, systems, and governance frameworks, with results measured against a control group.

To continue the conversation, contact us at [email protected].